Yesterday morning I walked down the street to the building with the big fat neon CHASE signs that replaced the modest old WaMu writing almost exactly two years ago, and did something that felt sooo good:

I closed my account.

Not only that, I found a friendly bank right up the street with a personable staff, a mission to support small and local businesses, environmentally conscious, where the manager brings you cookies baked on site with dough from Marin-based Homeward Bound, a non-profit agency known for assisting homeless people to learn career skills and find jobs.

When it comes to money I’m kind of old school — a one-bank kinda guy. I grew up in Germany where the local branch of our savings bank gave us kids little piggy banks to collect coins and the clerk’s kids were on my soccer team. Not to get too sentimental here, but there is something to be said about knowing that your bank is a part of your community and you can count on it (and its employees) to be there beyond the next boom/bust cycle.

That’s the general attitude with which I walked into a branch of a First Interstate Bank in 1987 to open my first checking account in the U.S. I picked it because it had the word “state” in it, something I guess feels attractive to me because it implies a certain stability and modesty, which is what I’m looking for in a bank. When First Interstate was gobbled up by CalFed a few years later, I was a bit puzzled how quickly and casually it all went down, but it still sounded like a semi-smallish and regulated institution and they kept on all the old staff, so I just went with it.

Another few years later I got notice that CalFed had been bought by CitiBank and that my checking account would be seamlessly transferred over within a month. Citibank??? Are you kidding me??? You mean that global behemoth of capitalism, the emblem of the concentration of wealth and power? The financial superbully that may as well be its own country? That Citibank?

As if that weren’t enough, they also “sweetened” their takeover with a monthly checking fee on the little guy, aka people who can’t keep a gazillion dollar minimum balance. I mean, shouldn’t it be the other way around, shouldn’t they charge their fees from people who have more than a certain amount in their account, the people who can actually easily afford the extra 10 bucks a month? Isn’t this whole idea of punishing those with little means the very mechanism by which the rich get richer and the poor stay poor?

This was the official end of my honeymoon with American banks. I mean, loyalty is a two-way street, isn’t it? While it’s a pain in the ass to close a bank account and having to switch over all your transactions, it’s a small price to pay compared to going over to the dark side and being milked for it to boost. So, I preempted the hostile Citi takeover and switched over to WaMu, who had free checking and at the time seemed like a fairly decent, community-oriented bank. One way for me to test out whether a business is on the right side of the fence is to get a feeling of how authentically psyched employees are about working there, and my local WaMu branch was filled with locals (I live in a predominantly Latino part of SF) and the atmosphere was really casual, family-style. No bullet-proof windows either, which was a big plus.

Then of course, as we all know, the great meltdown of 2008 happened and from one day to the next, WaMu was gone and within months my city started to look like this:

“Here we go again,” I thought to myself, but this time I didn’t even have a chance to think about it: before I knew it the only evidence left that WaMu had ever even existed was that rickety old checkbook in my drawer I was graciously allowed to use up. But, since Chase was keeping all the same terms and conditions for their WaMu customers at first and the takeover wouldn’t affect my personal little banking world, I thought, “okay, I’ll give this a chance for a while.” I admit, part of it was being too lazy to switch over all my bills again, and the convenience of shiny new ATM’s everywhere didn’t exactly help my state of being a bank sloth. They had me right where they wanted me.

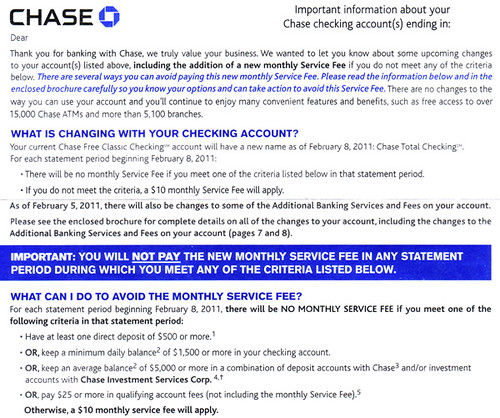

But thankfully, Chase took care of my inertia and my temporary subconscious denial that my mere existence as their customer, small as it may be, was feeding their ridiculous wealth and power, with all its repercussions. First they had their employees dress in ugly uniforms and put them back behind bullet-proof windows. Then they put in huge Vegas-style Brave New World video screens everywhere bombarding you with their own greatness. I guess it was bound to happen sooner or later, but the letter I got a few weeks ago announcing a $10 checking fee unless I keep a $1500 balance actually came as a nice kick in the butt, and ultimately, a relief:

So this seemed as good a time as any to really do some homework and find a bank or credit union that was aligned with my values and small and local enough that they wouldn’t just be gobbled up the next time Wall Street coughs. I’d done some research a while ago on banking and financial alternatives for a post entitled One Man’s Portfolio is Another Man’s Oil Spill, and so I started to study up on which of the many great alternatives out there would be the right one for me. I recommend the following links to anyone who is thinking about getting out of the big bank cycle and is looking for a place to start

Rethinking Money

Ultimately, we’ll have to rethink the way we trade goods and build nest eggs if we are to make it through climate change and peak oil and live in ecological balance with our planet. Some initiatives launched in the last year are gaining momentum around the country. The Slow Money movement looks at investment strategies revolving mostly around the world of local food and farming. The Move Your Money campaign was launched to help individuals and companies move their finances into local community banks and credit unions. The Common Good Bank is a new banking model where depositors decide what the bank should invest in. And a whole range of community currencies, barter and local exchange trading systems have sprung up around the world addressing the collective desire for more fair and just transactions based on direct interactions and actual value rather than speculation and quarterly earnings.

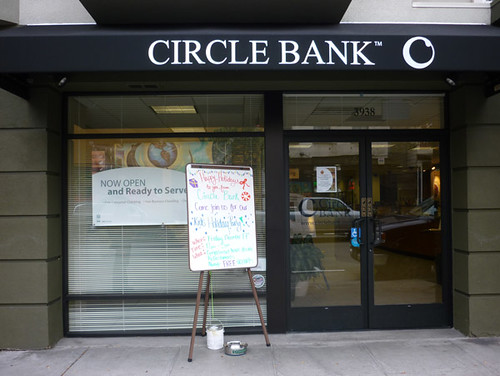

Eventually though, it was my partner Deb, who had also been Chased Away™, who suggested to walk up the hill to this new bank that had opened up a while ago, and check them out. Every time we’d walked by we thought it was pretty cool that they have stroller parking in that branch (even though we don’t have kids, but it’s such a nice touch). I know that’s not really what makes or breaks a bank, but walking into this setting makes you wonder whether your money might not be the one and only thing they’re after:

We were greeted by a friendly young woman named Rebecca, and after chomping down on some of the above-mentioned locally baked organic cookies, we got down to business. Not only did they offer free checking and savings accounts (and a free business account for Deb), but their business model and whole vibe was very much in tune with the things we care about: A small bank with only five branches spread across SF and the North Bay, with a deep commitment to investing in local businesses and non-profits, being engaged in the community, and sustainable practices. No big bureaucracy, shady foreign investments, mortgage deals, or credit-crushing monopolies. And thank heavens, none of those cringe-inducing, over-the-top chest-thumping supersize me antics.

Instead of this…

you get this…

In the grand scheme of things this is perhaps not that big a deal. I’m probably not going to stop this terrible and unsustainable economic system of ours that thrives on perpetual and misguided growth, rewarding the biggest and most ruthless players to accumulate more wealth and power than entire countries, by switching my measly little checking account. But every plant has to grow from a seed, and the more of these little seeds are sown the more likely they’re going to spread.

If nothing else, stepping into a bank with seven employees who are psyched about their work and have a stake in their company is like a breath of fresh air. You can just feel it, there’s something different about dealing with people who know what’s in their soup. After being slowly sucked into the cauldron of big-bank inevitability I feel like the bird that got out of the cage, and I’m really enjoying the view out here. There was just one last thing to do…

==============

to find a better bank and financial services near you, check out these resources:

Resources:

Responsible Credit Cards

Social Investment Forum

Slow Money movement

Move Your Money

Common Good Bank

Green Money Journal

Great article Sven! I was invited to become a member of a local credit union nearly 20 years ago. I decided to join because my own bank had just instituted checking fees based on low balances. It’s turned out to be a great relationship and a very cool, sustainable choice. Love the resources you shared, too!

Great to hear that, Tracie. We checked into some credit unions too around here, and there are some really good ones. Ultimately it came down to the proximity, being able to walk to our bank is huge. Also, Circle Bank offers a free business checking account, which was a big plus for Deb. And their commitment to investing in local non-profits really sealed the deal.

My bank is not horrible (yet) but this story makes me wish I could open an account at Chase just to experience the joy you did in closing it. 😉

I hope enough of the friendly community banks can stay in business so that we can find them when the inevitable fees start getting tacked on to our big-bank accounts.

Thanks for this post.

Jan, I actually hope there’ll be more and more of these community type banks. It seems that it’s a lot of the medium size banks that are getting gobbled up by the big boys, but I think the small authentic community types are somewhat immune to that. For one, they’re not worth pursuing for these mega banks, and also their very business structure doesn’t make them as susceptible to the whole Wall Street tango. Also, while these big banks always like to pretend to be interested in the community and spend lots of advertising dollars to create that impression, people who decide to go with a local bank for those very reasons know the difference and can’t be fooled. I think the key is not to make the small banks larger but to have many more of them and keep the playing field as local and diverse as possible. In a way that is mimicking a true ecosystem and the antidote to the current monolithic corpocrat system.

Your act itself may not make that big of a difference, but when linked to all like acts and by writing about it, it’s a pretty big deal. Thanks for the links, too.

Thanks Pam, I do agree that every small act makes a difference, it’s like spreading seeds. And I’m certainly not alone or the first one to do this, as those links show. It’s quite amazing and encouraging how many people are taking action on this. And it’s not hard to do at all or an inconvenience, that’s just what the big banks want us to believe.

When I read all those success driven prosperity mantra , I suppose that those who spread such concepts or fancy to join in those who “deserve more “, don’t want to think about the fact that wealth don’t fall from the sky, but is exploited out of other humans and resources.

But after all, I think that its simply an old con artist trick, catching flies with sugar water.We know who makes truly a profit out of the greed mentality of other.

Good you find an alternative. But lets remain attentive.We know from the micro credits in India , how good ideas can turn disastrously wrong.

The concept of plus value has to be deeply questioned as “useful tool” serving humanity.

Yes, it’s good to remain attentive to all the different layers of our human interactions. Too often we think we do something “good” but it’s only a one-dimensional good. So it’s important to learn as much as we can and as deeply about the mechanisms not only of the earth’s ecosystem, but of our human systems, financial and other, and how they’re interrelated with and affect the natural ecosystem. I’m not quite sure yet how much “good” my little switch has done or will do, but I thought it was worth the try. I will keep observing the effects of it and report back in a little while…

[…] is NOW to stop rewarding bankers for their very bad behavior. Please see this thoughtful article at World of Words about what banks should be and can be through supporting small people/businesses. And let us check […]

Wise man you are Sven.

Thanks for the post,

Mike

[…] my accounts at the bank from which I was Chased Away™, a phrase coined by my partner, Sven, in his blog post about how and why we moved our money to Circle […]

[…] move your money, you are joining a vast community of individuals, families, small business owners, nonprofits, and even cities who are choosing to bank with […]

A mutual friend of ours named Kirsten sent me your blog to read. Thank you so much for writing this and putting out this information. Very helpful for my present situation.

Thank you!

Tania

Thanks for stopping by Tania. Are you talking about Kirsten or Kirstin? Got two friends with slight variations on that name. : )

As far as the bank, over a year later I’m still super happy with Circle Bank, I don’t regret for a minute having left Chase. I don’t know where you live, but if there’s a small community bank or credit union in the neighborhood I highly recommend the switch. Your whole body will feel good. 😉

[…] I kept delving into themes from zero waste to renewable energy to community banking to the value of street food, my writing and storytelling became more fluent, confident, and […]

Hi Sven,

I really appreciate this post as I have been reading “socially responsible investing for dummies” and am on the search for a new bank. Do you have any insight as to what I should do as a just-graduated woman with a inclination to move and travel? I would like to open a community bank account but as I will likely not live in the same place for the next couple of years I am wondering how accessible my money will be. ie. where I can get cash out.

I found out about you in Yes! and wanted to learn more. I am also a blogger and feel that we share some values and ideas. I would love your feedback if you catch a moment at http://www.ispeakfortheseas.wordpress.com.

Thanks Sven!

Hi corallorax,

Yay, I love your blog, so cool, so deep, and so many of the same things that make your world go round, from ecovillages to world travel and being good to each other. I’ll definitely keep checking in, and can’t wait to hear about your upcoming travels. As far as a good bank that will also serve you well internationally, that’s a really good question. My experience has been that most debit cards with the magnetic strip work on ATMs abroad, so if you have an account with a smaller community bank in the U.S. it should work for you just as well as any of the big institutions. Either way, you will be charged a withdrawal fee, so you may as well pay the good guys. My Circle Bank card has worked pretty much anywhere, but incidentally Circle Bank just got bought up by Umpqua Bank, so here we go again, though Umpqua itself is fairly regional and still within what I’d consider acceptable size and ethics. I’m not sure what part of the country you are in, but if you’re already with someone you like I would ask them what their deal is with getting money from international ATMs.

Let me know what you find out, and good luck, happy trails, and big hugs to you.

Sven

Thanks for your warm and encouraging response. I think that is good advice about the banking. I will be looking around. Good luck with not letting your bank get gobbled up! I’ll be reading you 🙂